Calculating Stock Price: Detailed How-To

12 minutes for reading

Introduction

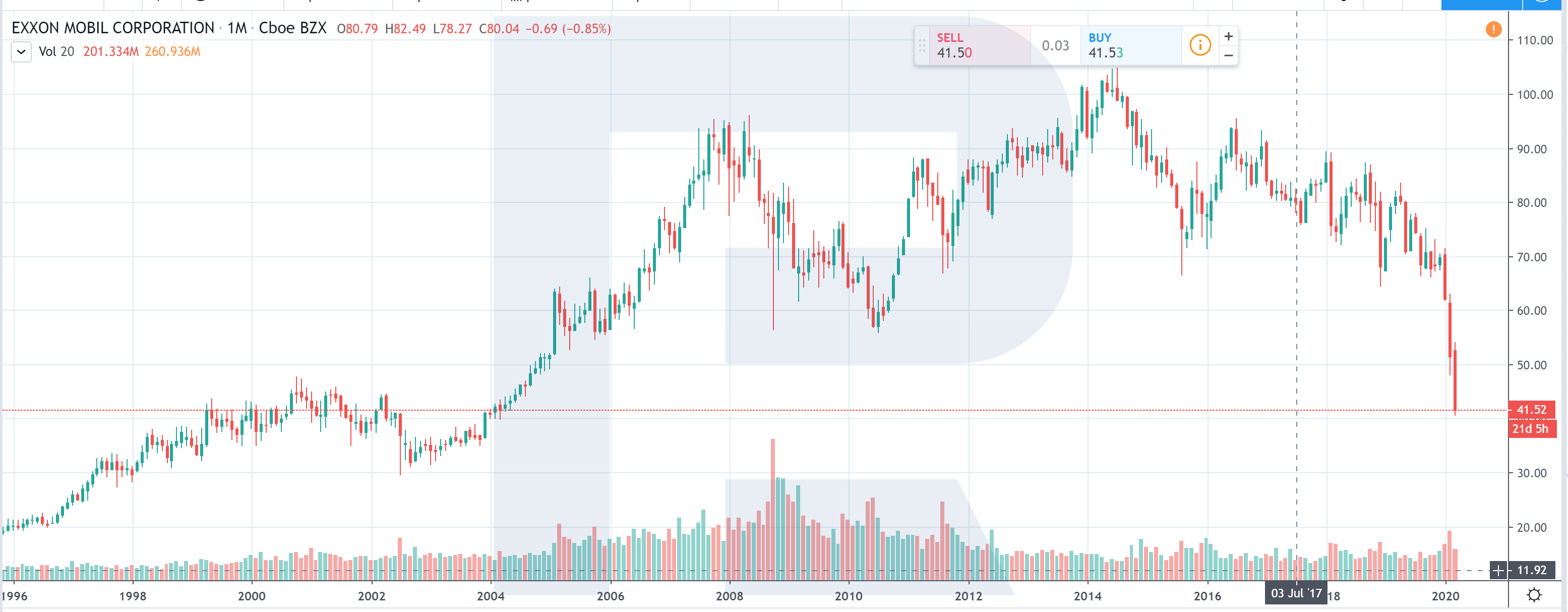

In the below chart, you may view the unadjusted (or nominal) daily closing price of the Exxon (XOM) stock since 1996.

This chart does not reflect the profit a trader would have made since 1996 – the changes in the nominal price only form one part of the investment results. Since 1996, Exxon has paid hundreds of dividends, which made the stock price decline every time. Also, Exxon carried out stock splits on five occasions, on which, its stock price shrank. Exxon acquired several enterprises and merged with Mobil Oil in 1999, which also affected the price of its stock. However, none of the actions above influenced the stockholders because the alterations remained purely nominal.

The time-series analysis of the stock price requires the adjustment for or elimination of such nominal changes. The historical stock price needs to be adjusted in such a way for the data received to represent the general profit the trader would have made if they have held a certain stock for a certain period. Through the adjustments, we create a series that reflects dividends, mergers, spin-offs, splits, and other actions affecting the factual profitability of the stock.

Any such event or a change in the company’s structure brings about discontinuous changes in the nominal stock price. Moreover, these changes are not due to the sellers or buyers repricing the company – they are corporate rather than market actions. The price adjustment is meant for the elimination of such actions.

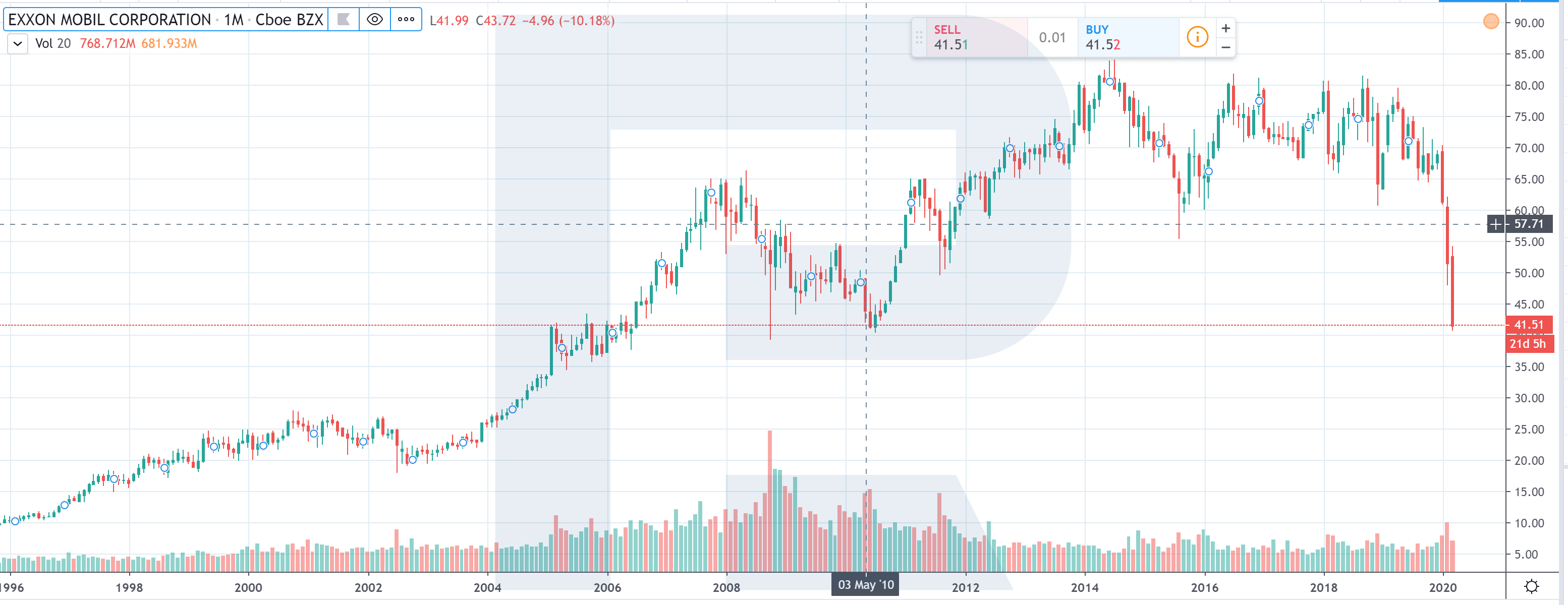

Below, you may also view the chart of the adjusted Exxon stock price since 1996. It differs dramatically from the first one, being much closer to the economic reality.

Any professional analyst knows that the analysis of the stock must be based on the adjusted stock price. However, only a few have the financial mathematics knowledge required for adjusting. Of course, you can always refer to some third party to give you the adjusted prices. Nevertheless, understanding how these adjustments are made is key to a successful analysis.

Principles of adjustment

Almost always, stock prices are backward adjusted. In other words, in every time series, the current day stock price is the same as the current price on the exchange. All adjustments are possible on historical data solely.

The adjustment of historical stock prices is normally multiplicative. Thanks to this, the profit from holding the stocks on the days when no adjustments have been made remains untouched regardless of all changes. Moreover, historically adjusted prices never turn out negative. However, some make additive adjustments, thereby triggering negative stock prices.

Below, we will discuss the most common corporate actions and their adjustments.

Cash dividends

When a company pays out dividends, the value of its share price declines. This is clear: the money is transferred from the company’s deposits to the clients, hence, the company costs this sum less. This means that, on the ex-dividend day, the stock price declines by the size of the dividend.

\begin{align}

\text{Share Price before Dividend} = \frac{\text{Company Value}} {\text{Shares Outstanding}} \\

\\

\text{Share Price after Dividend} = \frac{\text{Company Value – Total Cash Paid Out}}{\text{Shares Outstanding}} \\

\\

=\frac{\text{Company Value}}{\text{Shares}} \ – \ \frac{\text{Cash Paid Out}}{\text{Shares}} \\

\\

=\text{Share Price before Dividend – Dividend per Share}

\end{align}

To create a consistent time series of adjusted stock prices, we calculate the adjustment factor that reflects the decline of the stock price and thereafter divide the prices preceding the dividend payment by this factor.

\begin{align}

\text{Adjustment Factor} = \frac{\text{Close Price on Dividend Date + Dividend per Share}}{\text{Close Price on Dividend Date}}

\end{align}

As long as the adjustment factor is a multiplicative constant, it does not influence the profitability profile of the stock historically. At the same time, thanks to this factor, we may be sure that the calculated income on the dividend day is the consequence of real market actions and not the payment.

Let us have a look at the example of calculations with the adjustment factor after the dividend payment:

Apple (AAPL) paid out cash dividends of $0.47 per stock on 8 July 2014. On that day, the closing price was $94.48.

The adjustment factor is calculated as follows:

\begin{align}

\text{F} = \frac{94.48 + 0.47}{94.48} = 1.00497

\end{align}

The unadjusted closing price of the previous day was $94.96.

In this case, the adjusted closing price of the day before was:

\begin{align}

\text{P}_{adj} = \frac{\text{P}_{unadj}}{\text{F}} = \frac{94.96}{1.00497}=94.49

\end{align}

The price for all days preceding the payment is calculated in the same way (through multiplication by the factor), which gives us all the historical data of the “changes” brought about by the payment.

“Capital Repayments” and “Special Dividends” are special cases of cash dividend payments, in which the price is adjusted in the same way.

Stock dividends

Sometimes companies pay out dividends as additional stock instead of cash: each stockholder receives new stocks in proportion to what they already hold.

The idea behind this is to decrease the stock price. The price will be decreased in the proportion of the issued stocks to the existing ones. The overall cost of the company remains the same, while the price of the stock changes as long as the stock also changes. However, it should be noted that the ownership percentage and, hence, the cost of the stocks in dollars, which is held by each stockholder remains the same.

\begin{align}

\text{Share Price before Dividend} = \frac{\text{Company Value}}{\text{Shares Previous}} \\

\\

\text{Share Price after Dividend} = \frac{\text{Company Value}}{\text{Shares Previous + Shares Issued}}\\

\\

= \frac{\text{Company Value}}{\text{Shares Previous}} \times \frac{\text{Shares Previous}}{\text{(Shares Previous + Shares Issued)}}\\

\end{align}

As before, to create a consistent time series, we calculate the adjustment factor reflecting the decrease in the stock price and then divide the prices of the days preceding the dividend payment day by this factor. In this case, the adjustment factor is the second term in the equation above, hence, the dilution affecting the stockholders’ portfolios.

\begin{align}

\text{Adjustment Factor} = \frac{\text{New Float}}{\text{Old Float}}\\

\\

=\frac{\text{Shares Previous + Shares Issued}}{\text{Shares Previous}}\\

\end{align}

As before, as long as the adjustment factor is multiplicative rather than additive, it does not affect the profitability; it just “changes the scale”.

Let us look at the example of calculations with the adjustment factor:

On 3 December 2014, BIOL had a 0.5% stock dividend, meaning that a 0.005 (=0.5%) of stock was added to each stock already owned by the stockholder. In other words, one new stock was added for every 200 stocks in the portfolio.

Hence:

\begin{align}

\text{New Float} = \text{1.005} \times \text{Old Float}

\end{align}

Hence,

\begin{align}

\text{Adjustment Factor} = \frac{\text{New Float}}{\text{Old Float}} = 1.005

\end{align}

The unadjusted stock price on the pre-dividend day was 2.83.

So, the adjusted stock price on that day was:

\begin{align}

\text{P}_{adj} = \frac{\text{P}_{unadj}}{\text{F}} = \frac{2.83}{1.005} = 2.8159

\end{align}

Note that for these calculations, we do not use the closing price on the dividend day.

A stock dividend is sometimes called Bonus Issue.

Stock split

A stock split is like stock dividends. A stock split turns each existing stock into several stocks in a set proportion. This is identical to a stock dividends payment: stockholders receive new stocks in addition to those they are already holding.

For the stock split, the adjustment factor is calculated in the same way as for dividend stocks:

\begin{align}

\text{Adjustment Factor} = \frac{\text{New Float}}{\text{Old Float}}

\end{align}

Let us discuss an example of a stock split:

Chesapeake Utilities Corp. (CPK) had a stock split of 3 to 2, effective on 9 September 2014. Thus, instead of every two existing stocks, its stockholders received three.

In other words, one stock was added to every two stocks they already owned –this is absolutely equal to a stock dividend payment of 50%.

In this case,

\begin{align}

\text{New Float} = \frac{3}{2} \times \text{Old Float}

\end{align}

Hence:

\begin{align}

\text{Adjustment Factor} = \frac{\text{New Float}}{\text{Old Float}} = 1.5

\end{align}

The day before the split, the unadjusted stock price was 69.41.

Thus, the adjusted stock price on that day was:

\begin{align}

\text{P}_{adj} = \frac{\text{P}_{unadj}}{\text{F}} = \frac{69.41}{1.5} = 46.273

\end{align}

The stock split is also sometimes called Bonus Issue.

Reverse stock split

The reverse stock split differs from the common one in the sense that the stockholders do not receive more stocks; they receive fewer. Instead of increasing the number of stocks in the portfolio, a reverse split decreases it in a set proportion.

The stock price grows, as long as the overall number of stocks after a reverse split decreases. The cost of the company is not changed by this corporate action.

As before,

\begin{align}

\text{Adjustment Factor} = \frac{\text{New Float}}{\text{Old Float}}

\end{align}

Hence, the adjustment factor at a reverse stock split is less than one.

Let us discuss an example of a reverse stock split:

PostRock Energy Corp. (PSTR) carried out a reverse stock split in proportion of 1 to 10 on 1 May 2015.

\begin{align}

\text{New Float} = \frac{1}{10} \times \text{Old Float}

\end{align}

Thus:

\begin{align}

\text{Adjustment Factor} = \frac{\text{New Float}}{\text{Old Float}} = 0.1

\end{align}

The unadjusted stock price on the day before the reverse split was 0.4442.

Hence, the adjusted stock price:

\begin{align}

\text{P}_{adj} = \frac{\text{P}_{unadj}}{\text{F}} = \frac{0.4442}{0.1} = 4.442

\end{align}

The reversal stock split is also called Consolidation.

Adjustment challenges

A glance at the price adjustment process is enough to realise how much effort is required for the collection of bias-free, well-adjusted historical stock price data. Although essentially there is nothing complicated about it, nevertheless, the database creation process entails painstaking, tiresome work.

In 2015, there were only 20,000 dividend payouts – and these constituted only one type of corporate action. There are also splits, mergers, reverse splits, consolidations, acquisitions, rights issues, buybacks, treasury repurchases, etc. When any of these actions happen, all historical stock price data needs to be recalculated. This means recalculating many thousands of date rows (250 date rows per year) and OHLCV for each stock every day. And there are thousands of companies in the US public markets.

As such, maintaining the historical stock price database entails a great amount of work, which requires expertise and a lot of effort. This is why the market is dominated by only a small number of highly professional data providers – low professionalism means lost rivalry. In the world of stocks, similar to anywhere else, you get what you pay for.

Corporate events in R StocksTrader

If you are not already familiar with the multi-market trading platform R StocksTrader, the information on this page will help you find out more about it.

Long positions

A client who has an open long position on the ex-dividend day will have a sum equivalent to the paid dividend deposited into their account. The operation is reflected on the History page under Account Information – Cash Corrections.

Short Positions

A client who has an open short position on the ex-dividend day will have a sum equivalent to the paid dividend withdrawn from their free funds. The operation is reflected on the History page under Account Information – Cash Corrections.

Dividends procedure

The dividends process means depositing/withdrawal to/from the account on the ex-dividend date at 3 pm, server time. The operation is reflected on the History page.

For a Long position,

Cash Dividend Amount = Dividend per stock * Volume

Where

Volume = Contracts × Contract Size

For a Short position,

Cash Dividend Amount = (-1) × Dividend per stock × Volume

Where

Volume = Contracts × Contract Size

Stock Splits

In the case of a Stock Split, the necessary correction of the client’s position will be reflected in their trading account according to the split parameters.

The Split procedure is carried out on the server every day at 3 pm, server time. This operation deletes all active pending orders (Limit, Stop) on the stock.

For all open short and long positions, the weighted-mean price and general volume are calculated, respectively. A split happens, and a new price and volume are set. The information is assigned to the long and short positions with maximal volume, respectively. When there are fractional stocks in a trade, such stocks are eliminated and turned into a balance operation – the Split Cash Correction. The volume of other trades on the instrument is cleared and transferred to History.

are complex instruments and come with a high

are complex instruments and come with a high  of losing

of losing  rapidly due to

rapidly due to  . 69,88% of retail investor accounts lose

. 69,88% of retail investor accounts lose  when trading

when trading  with this provider. You should consider whether you understand how CFDs work and whether you can afford to take the high

with this provider. You should consider whether you understand how CFDs work and whether you can afford to take the high