Market Week Ahead (May 25–29): US Inflation, the Middle East and Oil

13 minutes for reading

Investor attention this week is firmly on US inflation signals and an assessment of global demand resilience. The appointment of Kevin Warsh as Fed Chair has already shifted market sentiment: the probability of a rate hike by December 2026 has surged to 70%, and the dollar continues to hold dominant ground. In this article we prepared an analysis of the week's key events — from the critical PCE report to decisions from Oceania's central banks. Inside, you’ll find technical reference points, key price levels, and the latest market sentiment across major assets.

In Brief

- Core PCE is due Wednesday, May 27 — the FOMC's primary gauge of US inflation.

- US GDP (Q1, advance estimate) — important for gauging the likely economic impact of the Middle East conflict.

- US Oil Inventories (May 27–28) — data will provide further insight into supply and demand dynamics amid ongoing geopolitical risks.

The final days of May could prove pivotal for Fed rate expectations and the dollar's trajectory. The main event of the week is the release of the US PCE — the Federal Reserve's preferred inflation gauge. Markets will also receive the preliminary Q1 US GDP estimate.

In Asia, attention shifts to Australian inflation and the Reserve Bank of New Zealand's rate decision. These events have the potential to drive volatility in AUD and NZD amid uncertainty over global demand and rate outlooks. Commodity markets will continue to monitor US oil inventories and the geopolitical backdrop.

Key Events of the Week

| Date | Event | Instruments | Importance |

|---|---|---|---|

| Wed, May 27 | US Core PCE | EUR/USD, Gold, US500 | ●●● High |

| Wed, May 27 | RBNZ Rate Decision | NZD/USD, AUD/NZD | ●●● High |

| Wed, May 27 | Australia CPI + China Data | AUD/USD, Copper | ●● Medium / High |

| Wed–Thu, May 27–28 | US Oil Inventories (API / EIA) | Brent, WTI, USD/CAD | ●● Medium |

Instant Access to Global Markets with RoboForex MobileTrader

27

May

Forecast

+0.3% m/m

Previous

+0.3% m/m

Why It Matters

PCE remains the Fed's primary inflation indicator. If inflation proves persistent, the market may push rate-cut expectations even further into the future. Additional attention is warranted as some Bloomberg economists already expect the Fed to hold rates at current levels through the end of 2026.

Market Reaction

A strong PCE alongside resilient GDP would support the US dollar and add pressure on gold and EUR/USD. Weak inflation or growth data would revive rate-cut expectations and weigh on the dollar.

Market Sentiment

Market consensus is moderately bearish on EUR and bullish on USD. Following a series of elevated inflation prints and Kevin Warsh's appointment as Fed Chair, investors are increasingly pricing in a prolonged period of high rates. The probability of a rate hike by December 2026 has approached 70%. Meanwhile, the market fears that a fresh energy price spike driven by the Middle East conflict could reignite inflation. If Core PCE comes in above expectations, interest rate expectations will shift even higher. This will strengthen the USD and increase pressure on gold and the EUR/USD pair. Softer data would trigger profit-taking on the dollar and a short-term recovery in risk assets.

Source: RoboForex. Past performance is not indicative of future results.

Key Levels — EUR/USD

| Level | Value |

|---|---|

| Resistance | 1.1660 / 1.1700 |

| Support | 1.1580 / 1.1550 |

| Target | 1.1550 |

27

May

Forecast

2.25%

Previous

2.25%

Why It Matters

The Reserve Bank of New Zealand will announce its rate decision on Wednesday morning, followed by a press conference an hour later. Markets will look for signals on how close the RBNZ is to ending its easing cycle. Commentary on domestic demand and inflation could generate additional volatility.

Market Reaction

Aggresive rhetoric from the RBNZ would support the New Zealand dollar. Cautious comments or an emphasis on downside economic risks could increase pressure on NZD. AUD/NZD is particularly sensitive to any divergence in tone between the RBA and RBNZ.

Market Sentiment

Market consensus — neutral-to-bearish on NZD. The market broadly believes the RBNZ's easing cycle is nearing its end. However, investors are not yet ready to price in a shift toward a expectations of higher rates, given weak domestic demand and slowing global growth. New Zealand's dependence on Chinese demand and broader risk appetite adds further downside pressure. If the RBNZ signals that a pause in rate cuts is approaching, NZD would receive strong support. In the event of cautious commentary, the market would quickly return to selling the New Zealand dollar.

Source: RoboForex. Past performance is not indicative of future results.

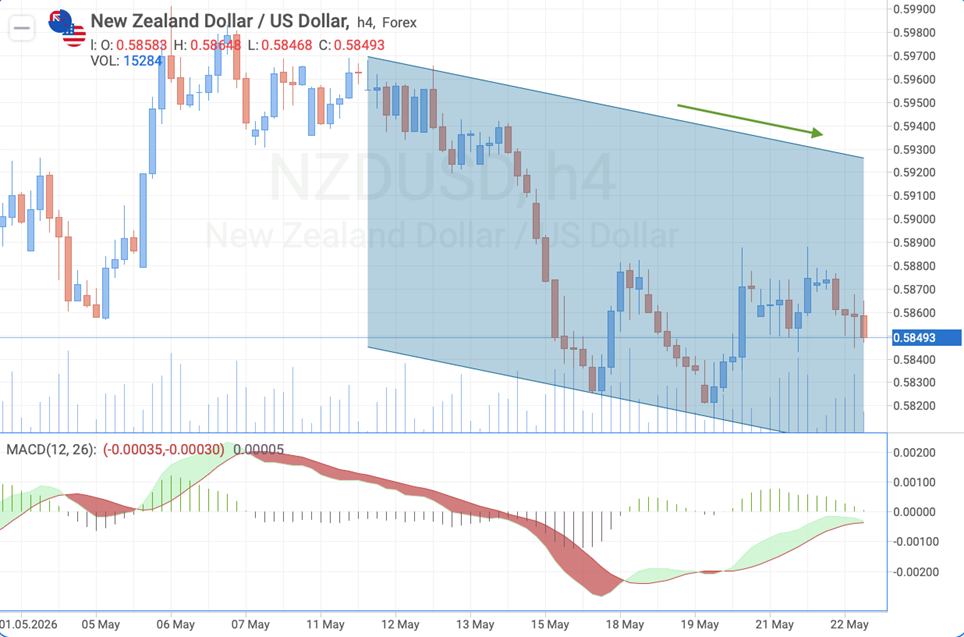

Key Levels — NZD/USD

| Level | Value |

|---|---|

| Resistance | 0.5930 / 0.5945 |

| Support | 0.5840 / 0.5820 |

| Target | 0.5820 |

27

May

CPI Forecast

+1.2% m/m (+5.1% y/y)

Previous

+1.1% m/m (+4.6% y/y)

Why It Matters

Australian data is particularly significant for AUD following recent swings in RBA rate expectations. At the same time, soft Chinese data could amplify concerns about global demand and serve as a reminder of the ongoing pressure on the commodity sector.

Market Reaction

Strong Australian inflation combined with stable Chinese data would support AUD and commodity assets. A weak Chinese data block would intensify pressure on commodity currencies. AUD/USD remains in a sensitive area following its spring recovery, while copper responds to signals of Chinese industrial activity.

Market Sentiment

Market consensus — cautiously negative on AUD and commodity currencies. Investors are sceptical about the durability of China's economic recovery, with recent industrial data from China appearing mixed. Meanwhile, some market participants are concerned that accelerating Australian inflation will limit the RBA's room for further rate cuts. If CPI comes in above expectations, the market may quickly revise its easing outlook — supporting AUD. Weak Chinese data, on the other hand, could intensify pressure on the Australian dollar, copper and other commodity assets.

Source: RoboForex. Past performance is not indicative of future results.

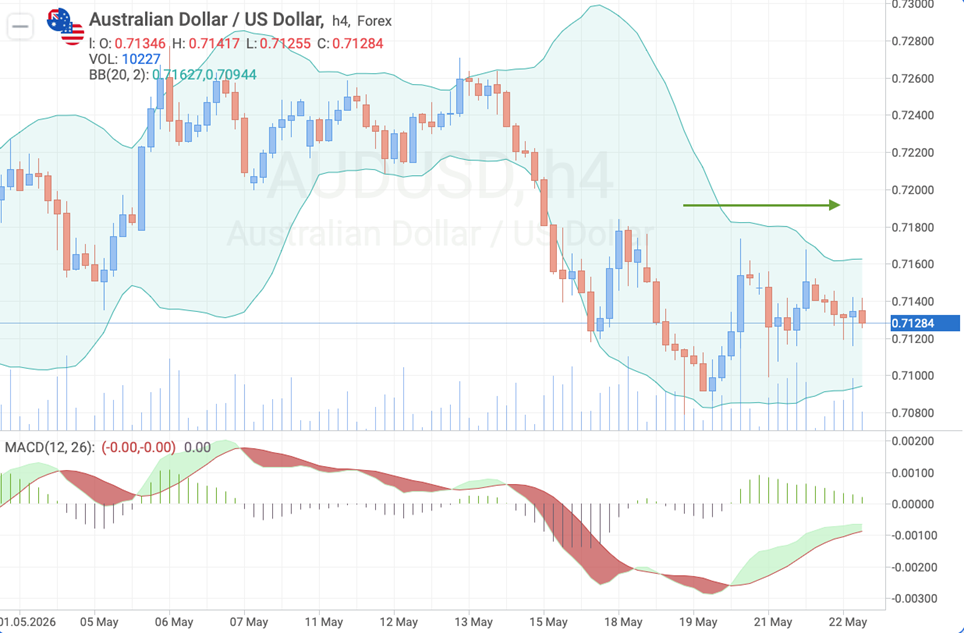

Key Levels — AUD/USD

| Level | Value |

|---|---|

| Resistance | 0.7180 / 0.7200 |

| Support | 0.7100 / 0.7080 |

| Target | 0.7180 |

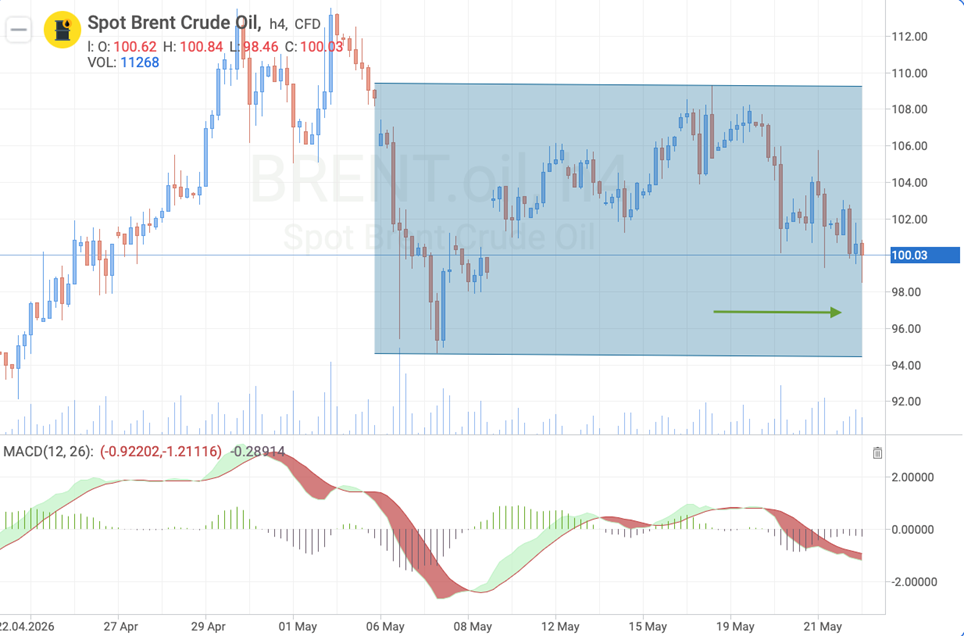

27–28

May

Why It Matters

The oil market continues to balance between geopolitical risks and fears of a global economic slowdown. Additional factors include news around the EU–Russia–Ukraine negotiation process and demand dynamics from China.

Market Reaction

A drawdown in inventories combined with rising geopolitical tensions would support Brent and WTI. Weak demand or a build in inventories could return downward pressure on oil prices. Brent remains dependent on the geopolitical news flow, while USD/CAD is sensitive to oil swings and US data releases.

Market Sentiment

Market consensus — moderately bullish on oil, but highly sensitive to geopolitics. Following the retreat of panic-driven expectations around the Middle East, part of the risk premium has already left Brent and WTI. Nevertheless, the market remains concerned about supply disruptions and further escalation. Additional focus rests on Chinese demand and signs of cooling in the US economy. If inventory data shows a sustained drawdown and the geopolitical backdrop stays tense, oil could resume its rally. An inventory build or deteriorating global demand expectations could quickly bring prices back under pressure.

Source: RoboForex. Past performance is not indicative of future results.

Key Levels — Brent

| Level | Value |

|---|---|

| Resistance | 102.00 / 108.00 |

| Support | 98.00 / 95.00 |

| Target | 96.00 |

Track forecasts and actual figures for each event — it is precisely the gap between expectations and reality that drives the magnitude of market moves. Learn more about how to read the economic calendar and trade the news.

Conclusion

The week centres on inflation signals and an assessment of global economic health. Wednesday's Core PCE sets the tone for Fed rate expectations — it is the key reference point for the dollar and risk assets in the weeks ahead. The RBNZ decision and Australian inflation will add volatility to the Asia-Pacific segment.

The key risk is inflation becoming entrenched against a backdrop of elevated oil prices and Middle East geopolitical tensions. This limits the Fed's room to ease policy and keeps pressure on risk assets. Warsh's appointment and the probability of a rate hike rising to 70% by December signal that markets are entering a new phase of tighter monetary policy.

Any information provided in articles on this website is based solely on the personal opinions of the authors. These articles should not be construed as trading recommendations or a call to action. The authors and RoboForex accept no responsibility for the results of any trades made on the basis of these recommendations and reviews. Past performance is not indicative of future results. Trading stocks and CFDs involves a high risk of capital loss.