Market Week (8–12 June): US inflation, ECB decision, and global economic signals

13 minutes for reading

Investor attention this week centres on US inflation, the ECB's rate decision, and an assessment of global economic momentum. Last Friday's jobs report reaffirmed labour market resilience, with 172,000 positions added against a forecast of 85,000, pushing back expectations of a near-term Fed rate cut. In this article we have prepared an analysis of the week's key events: from Tuesday's China trade balance to Friday's UK GDP, with Wednesday's CPI release at the centre of it all, a reading that will define the direction for the dollar and equity markets. Inside, you'll find technical analysis, key price levels and the latest market sentiment across major assets.

In Brief

- China trade balance — Tuesday, June 9. An early indicator of global demand and commodity currency conditions.

- US inflation (CPI) — Wednesday, June 10. The week's main event and key guide for Fed policy.

- ECB rate decision — Thursday, June 11. Key signals from Christine Lagarde on future policy direction.

- UK GDP — Friday, June 12. Assessment of British economic resilience for the Bank of England.

This week could prove pivotal for Fed rate expectations and broader risk sentiment. The main event is Wednesday's US CPI, the Federal Reserve's primary gauge of consumer price pressure. A reading above expectations would reinforce the case for rates staying higher for longer, while softer data would revive rate-cut hopes and provide support for equities.

Thursday's ECB rate decision adds a second major central bank event to the schedule. Markets will watch Christine Lagarde's press conference closely for signals on the pace of rate changes into year-end. China's trade balance on Tuesday and UK GDP on Friday round out a data-heavy week, with both capable of driving moves in commodity currencies and sterling.

Key events of the week

| Date | Event | Instruments | Importance |

|---|---|---|---|

| Tue, 9 Jun | China trade balance | AUD, NZD, copper | ●● Medium |

| Wed, 10 Jun | US inflation (CPI) | S&P 500, NASDAQ, USD | ●●● High |

| Thu, 11 Jun | ECB rate decision | EUR, DAX | ●●● High |

| Fri, 12 Jun | UK GDP | GBP, FTSE 100 | ●● Medium |

Instant access to global markets with RoboForex MobileTrader

9

June

Forecast

89.0 billion USD

Previous

84.82 billion USD

Why it matters

China remains one of the world's largest drivers of raw material demand and a crucial trading partner for most Asia-Pacific economies. Trade data lets us assess the state of global trade and domestic demand in the Chinese economy. This data is particularly significant for commodity currencies, including the Australian dollar, because Australia's economy is closely tied to China's industrial sector.

Market reaction

Strong trade data will support commodity currencies and improve sentiment on global growth. Weak statistics will intensify concerns about China's economic slowdown and pressure AUD and commodity assets.

Market sentiment

Market consensus remains cautious toward the Chinese economy. Despite some stabilization signals, the durability of domestic demand recovery remains uncertain. Concerns center on the real estate sector and mixed industrial production dynamics. If the trade balance comes in stronger than expected, markets may revise some negative outlooks on Asia's growth prospects.

Source: RoboForex. Past results do not guarantee future results

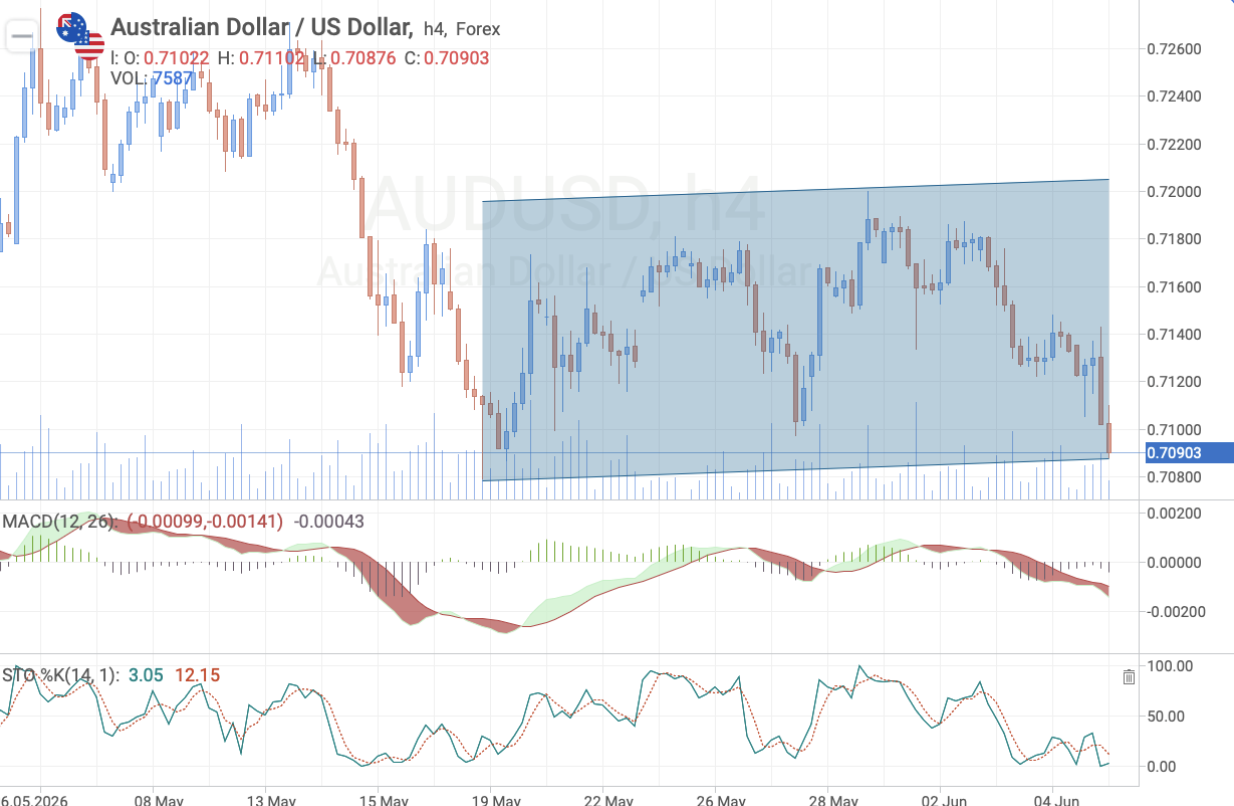

Key levels — AUD/USD

| Level | Value | Note |

|---|---|---|

| Resistance | 0.7140 / 0.7200 | Sell zone on strong data |

| Support | 0.7080 / 0.7060 | Lower boundary of range |

| Target | 0.7060 | Guide on weak China data |

AUDUSD continues trading within a wide sideways range that formed in late May. The MACD remains in negative territory and signals strengthening bearish momentum, while the stochastic hovers near oversold levels. Weak data from China could accelerate the pair's decline toward the range's lower boundary near 0.7060.

10

June

CPI (YoY) · Forecast

3.9%

CPI (YoY) · Previous

3.8%

Core CPI (YoY) · Forecast

2.8%

Core CPI (YoY) · Previous

2.8%

Why it matters

The CPI release will be the week's main event for global markets. Inflation remains the key factor determining the Fed's next moves. An acceleration in price growth will lead markets to price in sustained high rates for longer. Weak inflation will bring back discussions of potential policy easing in the future.

Market reaction

Higher inflation will increase pressure on equity indices and support the dollar. Weak data may improve risk appetite and support US equities.

Market sentiment

Market consensus remains moderately cautious. After several months of stubborn inflation, investors worry that bringing prices back to target levels may take longer than previously expected. Any signs of renewed inflation acceleration will trigger a revision of rate expectations and spark increased volatility across virtually all asset classes.

Source: RoboForex. Past results do not guarantee future results

Key levels — S&P 500

| Level | Value | Note |

|---|---|---|

| Resistance | 7600 / 7625 | Sell zone on inflation acceleration |

| Support | 7510 / 7450 | Holding zone within channel |

| Target | 7450 | Guide on profit-taking |

The S&P 500 remains within an uptrend channel, but sellers stepped up pressure last week. The MACD continues declining and signals negative momentum, while the stochastic stays near oversold levels. Higher US inflation could trigger profit-taking and push the index toward support at 7450.

11

June

Forecast

2.25%

Previous

2.00%

Why it matters

Markets will watch not just the rate decision itself, but also Christine Lagarde's comments on the future direction of monetary policy. For the euro, the key signals are whether the ECB will continue its rate-hiking cycle aggressively through the second half of the year. These forward-looking cues matter more for the currency than the decision itself.

Market reaction

Hawkish rhetoric will support the euro and temper expectations of further easing. Cautious comments could pressure the European currency.

Market sentiment

Market consensus remains moderately negative on the euro. Investors expect weaker economic growth in the eurozone compared to the US, which limits the potential for euro strength. Any signs of a harder ECB stance will trigger short covering of euro positions.

Source: RoboForex. Past results do not guarantee future results

Key levels — EUR/USD

| Level | Value | Note |

|---|---|---|

| Resistance | 1.1640 / 1.1700 | Upper range boundary |

| Support | 1.1580 / 1.1550 | Holding zone |

| Target | 1.1640 | Guide on hawkish ECB rhetoric |

EURUSD remains within recent weeks' range and is testing its lower boundary again. The MACD maintains negative dynamics, and the stochastic sits in oversold territory. As long as the pair stays below 1.1640, risks of further decline toward 1.1550 remain elevated.

12

June

Forecast

+0.1% m/m

Previous

+0.3% m/m

Why it matters

The report will assess the current state of the UK economy after mixed data in recent months. For the Bank of England, growth data remains a key factor in rate decisions. Markets will focus on signs of slowing business activity and consumer demand.

Market reaction

Strong GDP will support sterling and ease concerns about the economy. Weak data may boost expectations for softer Bank of England policy.

Market sentiment

Market consensus on sterling remains cautious. Traders acknowledge that the UK economy has proven more resilient than expected, but growth remains moderate. Any signs of slowdown will quickly bring back talk of the need for further policy support from regulators.

Source: RoboForex. Past results do not guarantee future results

Key levels — GBP/USD

| Level | Value | Note |

|---|---|---|

| Resistance | 1.3450 / 1.3560 | Zone for uptrend resumption |

| Support | 1.3400 / 1.3300 | Holding zone within channel |

| Target | 1.3450 | Guide on weak economy data |

GBPUSD continues moving within an uptrend channel, but buyers faced increased pressure in recent sessions. The MACD remains below the signal line, and the stochastic hovers near oversold levels. Weaker UK economic data will lead to testing support around 1.3300. For the uptrend to resume, the pair needs to close above 1.3450.

Watch how actual data compares to forecasts: the divergence between them determines the strength of market moves. Read more about how to interpret the economic calendar and trade the news.

Conclusion

The week revolves around inflation signals and global growth assessment. The CPI report on Wednesday sets the tone for Fed rate expectations, while the ECB decision and data from China and the UK round out the picture of major economies' conditions.

The week's key factor is inflation persistence in the US. Sustained price pressure limits room for Fed easing and supports the dollar, while slowing price growth could restore risk appetite for equities.

Any information contained in articles on this website is based on the personal opinion of the authors. These articles should not be considered as trading recommendations or a call to action. The authors of the articles and RoboForex bear no responsibility for the results of trades made based on recommendations and reviews. Past results do not guarantee future results. Trading stocks and CFDs carries a high risk of capital loss.