Oracle Stock Down 60% From Its Peak. Can the Bloom Energy Deal Trigger a Reversal in ORCL?

16 minutes for reading

Oracle has expanded its partnership with Bloom Energy, securing a supply of up to 2.8 GW of power units for its US data centre projects. For Oracle, the strategic value is clear: faster deployment of AI data centres means a quicker path to monetising the 553 billion USD in contracted backlog that the company has already signed.

In Brief

- Bloom Energy will supply up to 2.8 GW of power systems for Oracle's US AI projects.

- Oracle reseives a speed advantage over rivals in launching new AI data centres.

- Oracle is strengthening its competitive position in the AI market.

- 33 out of 42 analysts rate Oracle stock as a Buy.

- The 200-day Moving Average (MA200) signalling that the long-term uptrend remains active.

- Stochastic indicates a recovery in ORCL stock price is possible.

Trade Idea Parameters

Below are the specific parameters for the Oracle trade idea. The ticker for trading via RoboForex MobileTrader and MT5 on RoboForex is ORCL.

| Parameter | Value |

|---|---|

| Instrument | Oracle Corp (NASDAQ: ORCL) |

| Ticker in MobileTrader / MT5 | ORCL |

| Idea Date | April 21, 2026 |

| Time Horizon | 6–12 months |

| Direction | ↑ Buy (Long) |

| Entry Level (trigger) | 168 USD |

| Take Profit | 280 USD |

| Stop Loss | 148 USD |

| Position Size | No more than 3% of account · Medium risk |

Instant Access to Global Markets with RoboForex MobileTrader

The Deal Details

Against a backdrop of surging demand for cloud and AI computing capacity, Oracle and Bloom Energy have expanded their partnership under a new agreement by which Oracle will purchase up to 2.8 GW of Bloom's power systems. Of that total, the first 1.2 GW are already under contract — installation has begun and will continue into next year — with all units destined for Oracle's US-based projects.

For Oracle, this is a strategically important move. The company has stated publicly that demand for its AI capacity already exceeds current supply, while its contracted backlog has reached 553 billion USD. The faster Oracle can power its data centres and bring new capacity online, the faster it can convert that demand into real revenue.

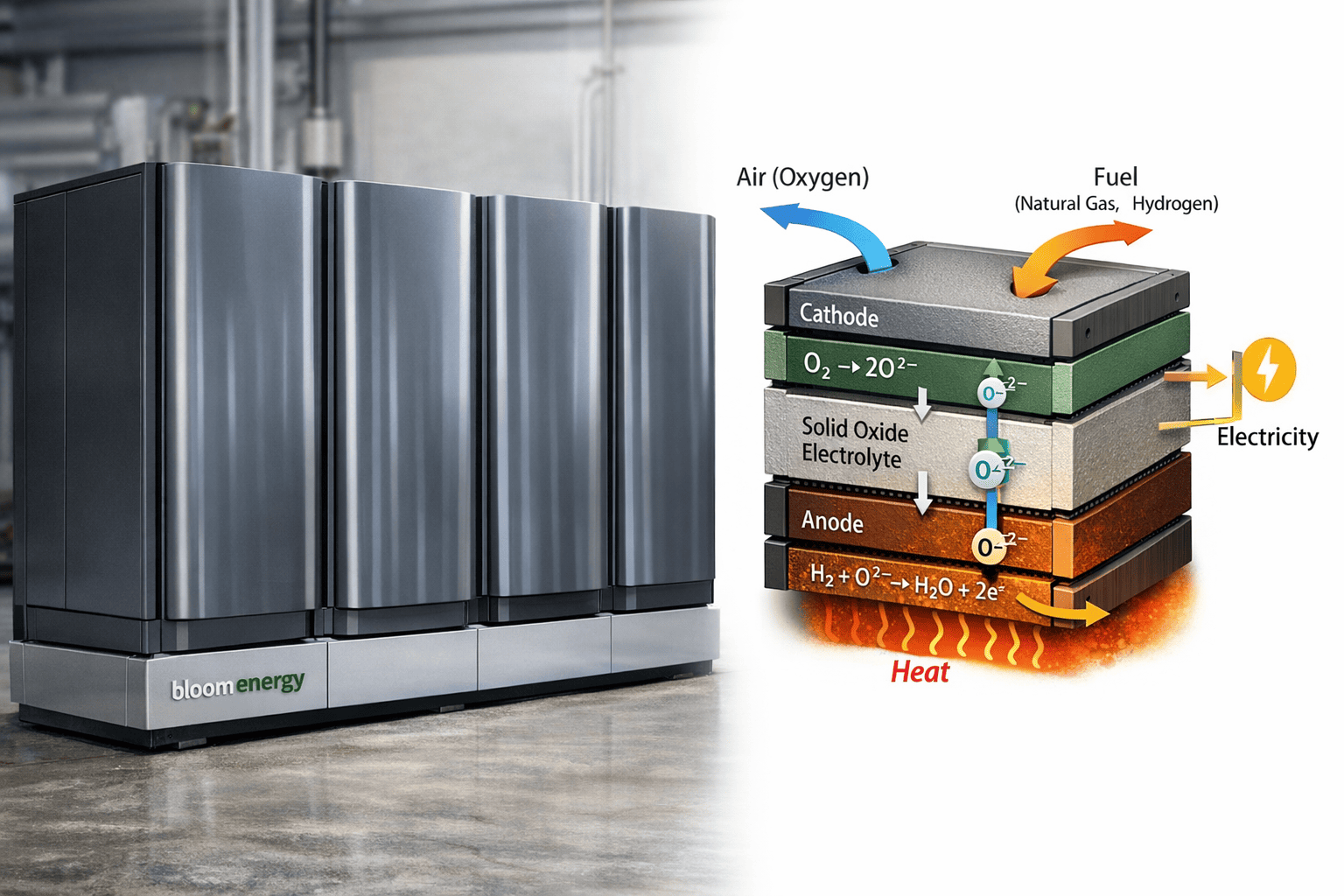

What Is a Bloom Energy Server

A Bloom Energy Server is a set of modular power units placed directly on-site next to a facility, generating electricity right where it is needed. Inside each unit, solid oxide fuel cells convert natural gas, biogas, or hydrogen into electricity through an electrochemical process. According to Bloom Energy's own data, the system runs continuously, requires no water during normal operation, and has already been deployed across more than 1,500 MW at over 1,200 sites worldwide.

One of the key advantages of the Bloom Energy Server is how quickly it can be deployed compared with conventional grid connections. Bloom says that in a previous Oracle delivery, the company had a fully operational system up and running in just 55 days — more than a month ahead of the originally expected 90-day timeline.

A second advantage is the system's ability to respond almost instantly to sudden spikes in power demand. In its own testing, Bloom demonstrated that its units can ramp load from 40% to 100% nearly instantaneously. Data centre experts have noted that AI facility power consumption can jump from 50% to 100% within seconds — and if the power source cannot keep up with that surge, it risks disrupting the entire site.

What Does Oracle Gain?

For Oracle, this deal is strategically valuable on several levels:

- Faster power delivery to new data centres. Access to electricity — and the time it takes to connect to the grid — has become one of the biggest bottlenecks for large data centres. Reuters has reported that even Google has called grid connection the single largest barrier to data centre expansion, with wait times in some regions stretching beyond a decade. On-site power generation lets Oracle bypass that queue entirely.

- Converting demand into revenue, faster. Oracle has said that AI demand continues to outstrip supply, and its contracted backlog now stands at 553 billion USD. That number means nothing until new capacity is actually switched on — so speed of deployment is critical.

- A stronger competitive position against AWS, Microsoft, and Google Cloud. For enterprise customers choosing between cloud AI providers, the ability to deliver ready capacity quickly is a real differentiator. If Oracle can launch new sites faster than its rivals, that becomes a tangible advantage when competing for large contracts.

In short, the Bloom Energy deal gives Oracle a tool for accelerating data centre construction. It helps the company bring new capacity to market sooner, reduces the risk of delays, and strengthens Oracle Cloud Infrastructure's competitive position in the race for AI.

Open a Trading Account at RoboForex

Swap-free accounts, spreads from 0, and execution in 0.01 seconds.

How Oracle’s 2.8 GW Stacks Up Against the Competition

The 2.8 GW contracted under Oracle's deal with Bloom represents capacity locked in through 2030 — a scale that puts Oracle firmly in the same league as the largest AI infrastructure projects in the market. For comparison, Google and NextEra already have around 3.5 GW of generation operating or contracted; Microsoft's data centre expansion in Wisconsin implies expected power demand of 2.6 GW by 2030; Amazon AWS is adding 2.4 GW through a new project in Indiana; and Meta's Hyperion project is being backed by three new gas-fired plants totalling 2.2 GW.

Against this backdrop, Oracle has joined the top tier of companies actively securing energy capacity ahead of future AI demand growth. This matters because in the years ahead, the pace at which AI businesses can scale will depend heavily on who has secured sufficient power supply in advance.

ORCL Analyst Ratings

As of April 2026, Barchart analyst ratings for Oracle stock reflect a strong consensus in favour of buying: 33 out of 42 tracked analysts rate ORCL as a Buy, 8 as Hold, and only 1 as Sell.

Buy — 33

Hold — 8

Sell — 1

33 out of 42

recommend Buy (79%)

Hold

8 (19%)

Sell

1 (2%)

Average Target Price

253.21 USD

Maximum Target

400.00 USD

Oracle Stock Technical Analysis

Oracle's capital expenditure jumped from 6.12 billion USD in fiscal year 2024 to 21.2 billion USD in fiscal year 2025, with the company planning to spend around 50 billion USD in fiscal year 2026. That means capex will have grown more than sevenfold over two years. At the same time, fiscal year 2026 revenue is forecast at 67 billion USD — a 26% increase over fiscal year 2024. The widening gap between spending growth and revenue growth unsettled markets, particularly against the backdrop of Oracle's plans to raise up to 50 billion USD in debt. The result was a sustained sell-off that took ORCL shares down roughly 60% from the September 2025 peak.

Despite that sharp decline, ORCL shares on the weekly timeframe continue to trade above the 200-day Moving Average, confirming that the long-term uptrend remains structurally intact. Since February 2026, the stock has been consolidating between roughly 140 and 158 USD, which signals that the downward momentum is fading and a base is forming. The Stochastic indicator is in oversold territory — a signal that suggests a potential recovery in ORCL may be ahead.

The base-case scenario points to a breakout above the 20-day Moving Average near 168 USD as the entry trigger for a buy. The first upside target is the resistance at 220 USD; a confirmed break above that level opens the path toward the primary target at 280 USD. A break below the 140 USD support would invalidate the bullish setup.

- The 200-day Moving Average (MA200) has not been breached, confirming that the long-term uptrend remains in place despite the significant drawdown.

- Stochastic is in the oversold zone, indicating a potential resumption of the upward move within the long-term trend.

- A breakout above the 20-day Moving Average (MA20) near 168 USD will serve as the buy signal.

- First upside target: resistance at 220 USD. Primary target: 280 USD.

Sample Trading Strategy for Oracle Stock

Below is a sample trading strategy for ORCL shares. This example is for educational purposes only and does not constitute investment advice. Investors should assess their own risk tolerance independently.

| Parameter | Value |

|---|---|

| Entry Point | Breakout above the 20-day Moving Average at 168 USD per share |

| Take Profit | Resistance level at 280 USD per share |

| Stop Loss | Break below 140 USD — cancels the bullish signal |

| Risk / Reward Ratio | 1 : 4 — potential profit is roughly 4× the risk |

| Position Size | No more than 3% of account |

Sample Calculation for 10 ORCL Shares

| Scenario | Calculation | Result |

|---|---|---|

| Buy 10 shares at 168 USD | 10 × 168 USD | 1,680 USD |

| If target reached (280 USD) | (280 − 168) × 10 | +1,120 USD (+66.7%) |

| If stop triggered (140 USD) | (168 − 140) × 10 | −280 USD (−16.7%) |

| Risk / Reward | 280 / 1,120 | 1 : 4 |

A risk/reward ratio of around 1:4 sits comfortably in the acceptable range for position trading. Keep in mind that markets are volatile: ORCL shares can move both for and against an open position.

Trade with RoboForex MobileTrader

Live charts, deposits and withdrawals, analytics and copy trading — all in one app.

Risks

Like any trade idea, this scenario carries key risks that must be considered before making a decision.

- Execution risk. Even with the Bloom Energy agreement in place, Oracle still needs to prepare sites, install equipment, and bring new data centres online without technical delays. If infrastructure expansion moves more slowly than expected, the company may not be able to translate high demand into real revenue as quickly as the market anticipates.

- Gas dependency and energy infrastructure risk. Bloom Energy's systems rely heavily on gas supply, which means Oracle remains sensitive to fuel costs, supply disruptions, and potential changes in energy regulation. This creates an external risk factor that Oracle does not fully control.

- Competition. AWS, Microsoft, and Google are also actively securing large-scale power capacity for their AI infrastructure. The Bloom Energy deal gives Oracle an opportunity to accelerate its build-out and strengthen its position — but the race for the AI market remains intensely competitive, and the outcome is far from certain.

Conclusion

The Oracle and Bloom Energy agreement directly addresses one of the AI industry’s most critical bottlenecks: securing sufficient power for new data centres. By locking in up to 2.8 GW of capacity, Oracle gains a speed advantage in bringing facilities online and reinforces its competitive standing against AWS, Microsoft, and Google Cloud.

For ORCL stock, this means the company is better positioned to convert its 553 billion USD contracted backlog into real revenue. Investor attention will remain focused on the pace of spending, since capital expenditure is growing far faster than revenue. If Oracle demonstrates that new capacity is genuinely translating into earnings, that could become a powerful catalyst for further recovery in the share price.

From a technical perspective, ORCL shares are holding above the 200-day Moving Average — a sign that the long-term uptrend is active. The Stochastic indicator in oversold territory suggests the correction may be coming to an end. A breakout above the 20-day Moving Average near 168 USD could serve as the signal for a renewed move higher, with initial targets at 220 USD and the primary target at 280 USD.

* The information in this article reflects the personal opinions of the authors. It should not be construed as trading advice or a call to action. The authors and RoboForex bear no responsibility for trading results based on the recommendations and reviews contained in this material. Past performance is not a guarantee of future results. Trading stocks and CFDs involves a high risk of capital loss.